Operating, investing, financing, income taxes, and discontinued operations, with two mandatory subtotals: operating profit and profit before financing and income taxes. Standardized definitions replace the historical diversity in how groups presented their P&L.

Define and disclose MPMs in audited financial statements, ending the era of unaudited 'non-GAAP' metrics. Each MPM must be reconciled to IFRS-defined subtotals – with full transparency on tax effects and non-controlling interest impacts – and is subject to external audit scrutiny.

Interest paid moves to ‘financing’. Interest and dividends received move to ‘investing’. There will be no more optional treatments: every item must be classified consistently across the group, with no exceptions.

Functional presenters must disclose five natural expense categories. FX differences are now split by the underlying transaction type, while stricter aggregation principles eliminate vague line items.

Rule-based classification engine

Operating, Investing, Financing rules are defined once, enforced group-wide, and fully auditable.

Integrated MPM workspaces

Built-in reconciliation from every MPM to the nearest IFRS subtotal, with an approval workflow before external publication.

From close to disclosure

Consolidated data flows seamlessly to disclosure. Numbers and narrative stay consistent – from financial statements to your annual report.

Audit ready by default

Every classification decision documented. Full version history. Drill from any subtotal to the source transaction.

Your ERP handles transactions. IFRS 18 requires a consolidation layer that applies classification rules, manages parallel frameworks, and produces required reconciliations. Lucanet acts as that layer without touching your ERP.

Any non-IFRS financial measure communicated publicly that isn't a subtotal required by IFRS 18 counts as an MPM. Metrics like adjusted EBITDA, and underlying operating profit now require a formal reconciliation to the nearest IFRS 18 subtotal, within audit scope.

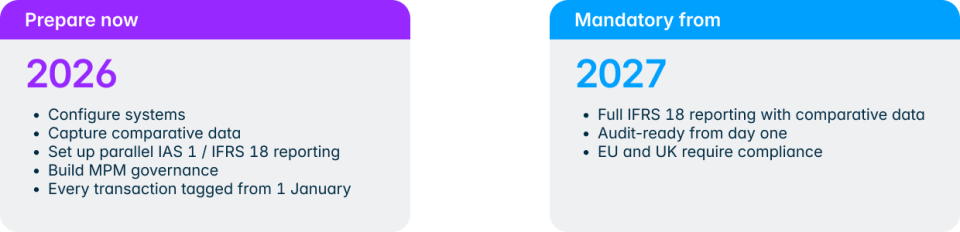

Yes, the restatement of obligation isn't limited to year-end reports. Interim financial statements throughout 2027 also require restated 2026 comparatives under IFRS 18. This means your systems need to be capturing IFRS-18-compliant data from 1 January 2026, not just for the annual close.